Filing a roof insurance claim in Kerrville, TX after a storm involves four key steps: documenting the damage, opening the claim, attending the adjuster visit, and reviewing the settlement offer. The process can feel complicated, but knowing what to expect at each stage puts you in a much stronger position. All Weather Roofing & Remodeling has been helping Hill Country homeowners navigate this process since 1989, and this guide breaks it down step by step.

Understanding Your Policy Before You File

Before you pick up the phone to call your insurance company, it’s worth spending 15 minutes reviewing your homeowners policy. Two terms matter most when it comes to roof claims:

Replacement Cost Value (RCV) means your insurance company will pay to replace your damaged roof with materials of like kind and quality at today’s prices, minus your deductible.

Actual Cash Value (ACV) means your insurance company will pay the depreciated value of your roof — what it was worth at the time of the storm, not what it costs to replace it today. On an older roof, this can be a significant difference.

Most standard homeowners policies in Texas offer RCV coverage, but some have shifted to ACV for roofing specifically, particularly after the high volume of hail claims the state has seen over the past decade. Knowing which you have changes your expectations going into the claim.

You’ll also want to note your deductible. Texas policies often have a separate wind and hail deductible that is calculated as a percentage of your home’s insured value rather than a flat dollar amount. On a $300,000 home with a 2% hail deductible, you’re responsible for the first $6,000 before insurance pays anything.

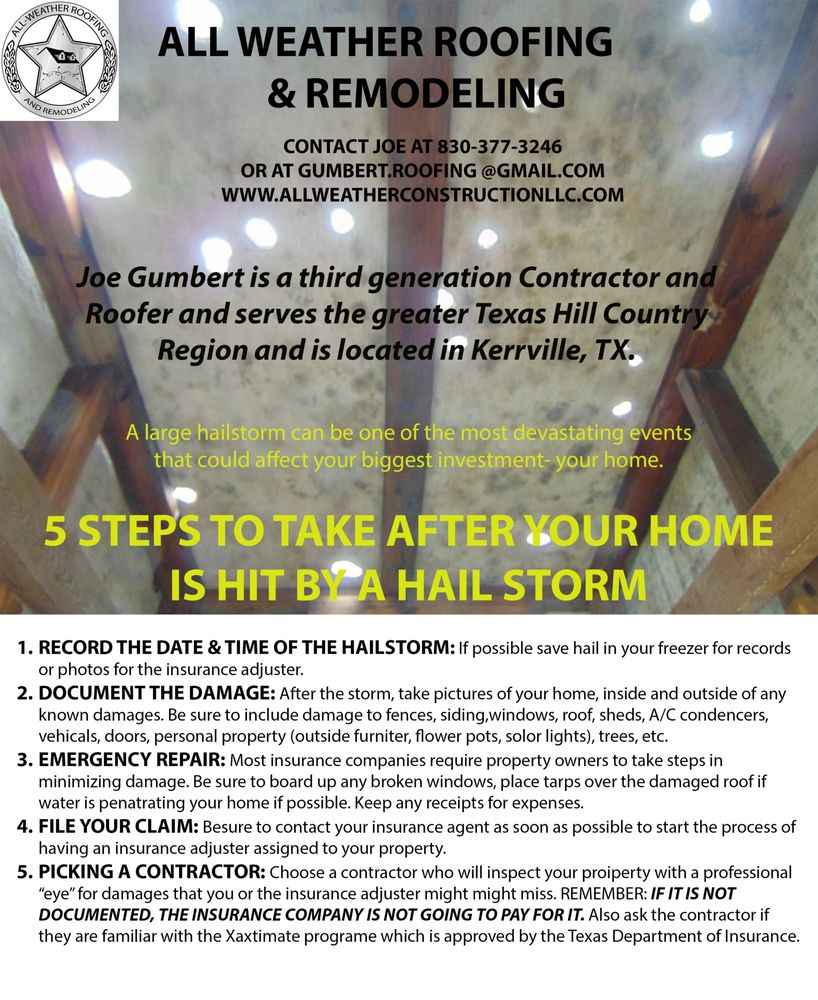

Step 1: Document the Damage Before Calling Your Insurer

The single most important thing you can do before filing a claim is document the damage thoroughly. Take photos and video of everything you can safely access — gutters, siding, window screens, exterior trim, and any interior water damage. Note the date of the storm and save any weather alerts or news reports from that day.

If you haven’t already, schedule a professional inspection with a licensed roofing contractor before the adjuster visits. A contractor’s inspection report gives you an independent assessment of the damage that you can compare against the adjuster’s findings. Our team provides free hail damage inspections for homeowners throughout Kerrville and the surrounding Hill Country. Learn more about what to expect during a hail damage inspection.

Step 2: File Your Claim Promptly

Once you’ve documented the damage, contact your insurance company to open a claim. Most insurers allow you to file online, by phone, or through a mobile app. You’ll receive a claim number and be assigned an adjuster.

Under Texas law, insurance companies have 15 business days to acknowledge your claim and 15 business days to accept or reject it after receiving all required documentation. Keep a written record of every communication — dates, names, and what was discussed.

One important note: filing a claim does not obligate you to accept the settlement offer. You can file, receive the adjuster’s assessment, and then decide how to proceed based on whether the offer is fair.

Step 3: The Adjuster Visit — What Really Happens

The adjuster’s job is to assess the damage and determine what your insurance company owes you. Their job is not to advocate for you. They work for the insurance company, and their estimates are often conservative.

This is where having a contractor present makes a significant difference. When our team attends the adjuster meeting with you, we walk the roof alongside the adjuster and point out damage that might otherwise be overlooked or attributed to normal wear. We speak the same technical language adjusters use, and we know what documentation is required to support specific line items in the estimate.

Common areas where adjusters undercount or miss damage include:

- Soft metal components like pipe boots, ridge vents, and flashing

- Granule loss on shingles that doesn’t yet show visible cracking

- Damage to siding, window screens, and exterior trim

- Code upgrade requirements that must be included in the replacement estimate

Having a licensed contractor at the adjuster meeting is one of the most effective ways to protect your claim. We do this regularly for Kerrville homeowners at no added cost.

If the adjuster’s estimate comes in lower than expected, you have the right to dispute it. We help homeowners prepare supplemental claims that document additional damage or correct undervalued line items. This process, called a supplement, is common and legitimate — it’s not confrontational, it’s just making sure the estimate reflects the actual scope of work.

Step 4: Understanding the Settlement Offer

Once the adjuster completes their assessment, your insurance company will issue a settlement offer. If you have RCV coverage, the initial payment is typically the ACV amount — the replacement cost minus depreciation. The remaining depreciation is held back and released once the repairs are completed and you submit proof of completion.

This two-payment structure catches many homeowners off guard. You receive a check that seems low, use it to start repairs, and then receive the remaining depreciation holdback after the work is done. Understanding this process upfront prevents confusion and helps you plan your project timeline.

Your deductible is subtracted from the total settlement. You are responsible for paying your deductible directly to your contractor — it is not paid to or through the insurance company.

What If Your Claim Is Denied?

Claim denials happen, and they’re not always the final word. Common reasons for denial include:

- The adjuster determined the damage was due to wear and tear rather than storm impact

- The damage was below the deductible threshold

- The claim was filed outside the policy’s reporting window

If your claim is denied and you believe the denial is incorrect, you have several options. You can request a re-inspection, hire a public adjuster to represent you independently, or invoke the appraisal clause in your policy, which brings in a neutral third-party umpire to resolve the dispute.

We’ve helped Kerrville homeowners successfully appeal denied claims by providing detailed contractor documentation that contradicted the adjuster’s initial findings. If you’re facing a denial, reach out to our team before accepting it as final.

Why Working With a Local Contractor Matters

National roofing companies that follow storm systems from state to state are a real concern in Texas after major hail events. These companies often pressure homeowners to sign assignment of benefits agreements, which transfer control of the insurance claim to the contractor. This can leave homeowners with little recourse if the work is substandard or the claim is mishandled.

All Weather Roofing & Remodeling is a Kerrville-based, family-owned business that has been serving this community since 1989. We don’t chase storms. We live here. Our reputation is built on the relationships we’ve maintained with Hill Country homeowners over three generations, and we have no interest in cutting corners or rushing through a job to move on to the next market.

When you work with us, you stay in control of your claim. We advise, document, and advocate — but the decisions are always yours.

Services That May Be Part of Your Claim

Depending on the extent of the storm damage, your claim may cover more than just the roof. Our team handles:

- Storm damage restoration for roofs that need full assessment and repair coordination

- Roof repairs for targeted fixes to leaks, flashing, and damaged sections

- Roof replacement when damage is too extensive for repair

- Siding repairs for hail-damaged exterior panels

- Window installation when frames or glass are compromised

Documenting all storm-related damage in a single claim is almost always more efficient than filing separate claims for different components. We help you build a comprehensive damage report that covers every affected area of your home.

Schedule a Free Consultation

If you’ve recently experienced storm damage and aren’t sure where to start with your insurance claim, we’re here to help. Our team will inspect your property, document the damage, and walk you through the claims process from start to finish — at no obligation.

Contact All Weather Roofing & Remodeling to schedule your free consultation in Kerrville, TX and the surrounding Texas Hill Country. Call us at (830) 377-3246.

External Links: